My summary of Venture Markets in Nov 2022:

Series B and later even worse than looks in data:

85%+ of investing here has simply ceased

Seed and Early Series A:

Deals take longer but off about 40%. Some have slowed down but most vets don't care too much about today's macros.

— Jason

Be Kind

So we’ve talked about it often here at SaaStr, but things are just so … odd right now in SaaS. The best are still growing, if not faster than ever, then still close to it. And while AWS’s growth is down a bit, it’s still at epic levels, Azure isn’t even really down, and Google Cloud is growing faster than ever. It’s still close to the best times ever in SaaS for growth and customers, even with mixed signals in the economy.

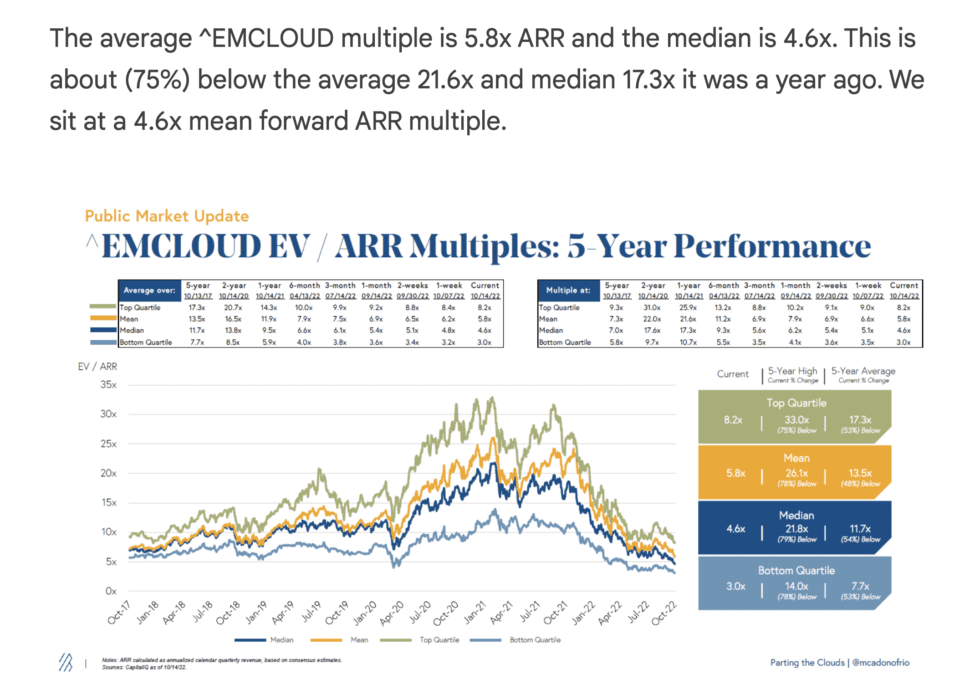

And yet … the stock markets have plummeted. Cloud stocks are down 50%, and multiples are down 75%, from their peaks.

The latter is the most important for raising venture capital. Valuations are down a stunning 75% from their peak last year. It took a quarter or two to sink in in venture, but now the effects are clear:

- Much of the growth market (Series B and later) has simply stopped investing, period. They are still looking for an outlier deal, something growing at such insane rates it clearly will be worth $10B+ even in today’s world, but other than that, growth is mostly on hold.

- The Series A market is still alive, but with Series B on hold, there is little appetite for high burn rates and “next round risk”. Series A rounds are much harder to close, not just because valuatiosn are down, but even more because there’s no Series B backstop coming. The money may have to last … forever.

- The Seed market in Venture is active, mainly because it can go long. But only up to a point. Seed investors have such long time horizons that they expect up and down markets. But … they still need the Series A, B and C markets to carry the ball down the field. With those markets much tighter, and even frozen, it puts a lot of pressure on. Seed investors are looking for folks that are more capital efficient. And inherently expecting more of them to fail due to lack of next round capital.

Sam Blond, ex-CRO at Brex and the newest Partner at Founders’ Fund and I did a deep dive here:

Even at Founders Fund, which takes big risks on Decacorns, growth investing is awfully … quiet. It’s very, very quiet at $300m+ valuations. And even if you are raising at a $3m valuation, that’s going to impact you.

The bottom line is this, and I think it’s the one message most founders haven’t heard yet. They get things are tougher, that venture has changed. What they don’t get is this. Today, you just have to assume the next round isn’t coming. At least until you are 90%+ sure you’ve got a real VC that wants to lead the next round, for sure.

That’s the way it used to be. I remember when my Series Seed investor told me this back in the day, and it sunk in. “Assume there’s no more money coming.”

This generally means your capital will have to stretch twice as long as you’d planned. It can often be a big bummer.

But right now, it’s just prudent to assume the next round isn’t coming. It almost certainly isn’t, for now, at Series B or later. That makes Series A much harder. And so on.

The post Founders Today Just Need to Assume the Next Round Never Comes appeared first on SaaStr.

via https://www.aiupnow.com

Jason Lemkin, Khareem Sudlow